Free North Dakota 307 Template

Free North Dakota 307 Template

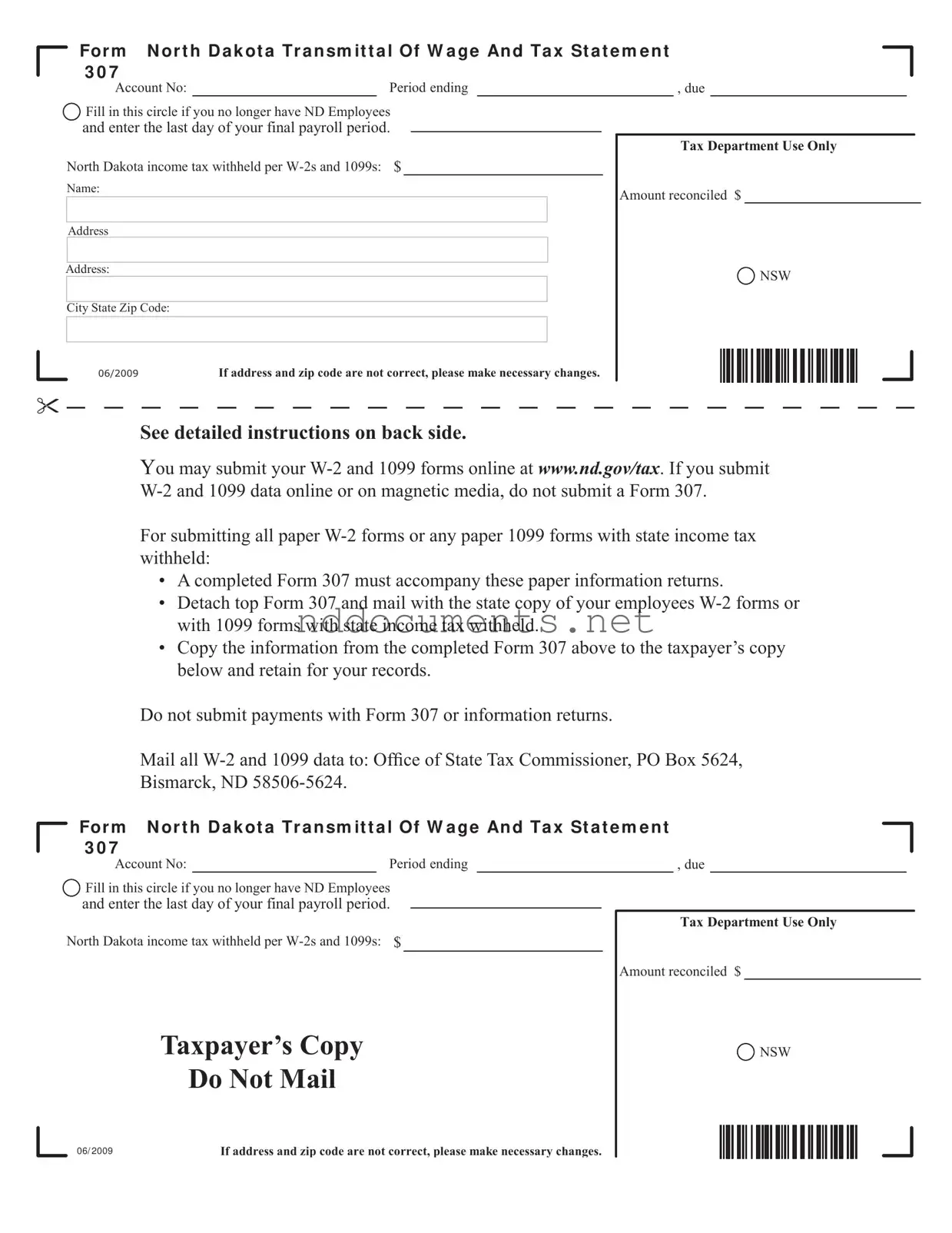

The North Dakota 307 form serves a crucial role in the state's tax system, particularly for employers and individuals who have withheld state income tax from wages or payments. This form is required for submitting W-2 and 1099 information returns to the North Dakota Office of State Tax Commissioner. When filing, employers must report the total amount of North Dakota income tax withheld, as indicated on the W-2s and 1099s. If an employer no longer has employees, they must indicate this by filling in a specific circle on the form and providing the last payroll date. Additionally, it’s essential to ensure that the name and address on the form are accurate to avoid complications. For those submitting paper forms, a completed Form 307 must accompany each W-2 and 1099 that reports state income tax withheld. Notably, if the number of forms exceeds 250, electronic submission is mandatory. Understanding the requirements and deadlines for filing this form is vital, as it must be submitted by February 28 of the following year if the business is still operational. For businesses that have closed, the form should be submitted alongside the final federal forms. This introductory overview highlights the significance of the North Dakota 307 form in maintaining compliance with state tax regulations.

When dealing with the North Dakota 307 form, it’s essential to understand the requirements and procedures to ensure compliance. Here are some key takeaways:

By adhering to these guidelines, you can navigate the filing process more effectively and avoid potential issues with state tax compliance.

| Fact Name | Description |

|---|---|

| Purpose | The North Dakota 307 form is used for submitting wage and tax information for employees, specifically W-2 and 1099 forms, to the state tax authorities. |

| Filing Requirement | Employers must file Form 307 if they are subject to North Dakota's income tax withholding law, regardless of whether they withheld tax. |

| Submission Deadline | W-2 and 1099 data must be filed by February 28 of the following year if the business is still operational. |

| Final Payroll Notification | If an employer no longer has North Dakota employees, they must indicate this on the form and provide the last payroll date. |

| Electronic Filing | Employers must file electronically if they are required to do so by the IRS and have 250 or more forms to submit. |

| Tax Withholding Reporting | The total North Dakota state income tax withheld must be reported on Form 307, based on the amounts shown on W-2s and 1099s. |

| Governing Law | Form 307 is governed by North Dakota Century Code § 57-38-58, which outlines the requirements for income tax withholding and reporting. |

When filling out the North Dakota 307 form, it is essential to follow certain guidelines to ensure accuracy and compliance. Below is a list of important dos and don'ts to consider.

By adhering to these guidelines, you can help ensure that your submission is processed smoothly and efficiently. If you have any questions or need further assistance, consider reaching out to the appropriate tax office for guidance.

The North Dakota 307 form is a critical document for employers in North Dakota who need to report wage and tax information. Along with this form, there are several other documents that may be required for proper tax reporting and compliance. Below is a list of forms and documents that are often used in conjunction with the North Dakota 307 form.

Understanding these forms and documents can help ensure compliance with North Dakota tax regulations. Proper filing can prevent penalties and ensure that all tax obligations are met accurately and on time.

North Dakota Income Tax Calculator - The T 12 form must include accurate contact information for the reporting entity.

To begin your homeschooling journey in Arizona, it's important to understand the significance of the document known as the Homeschool Letter of Intent. This form facilitates the official recognition of your homeschool setup, aligning with state educational requirements. For further guidance, refer to this procedure for completing your Homeschool Letter of Intent correctly.

North Dakota Nonresident Filing Requirements - Detailed instructions guide fiduciaries in proper form completion.